An average household has a credit card debt of £2,572, and personal loan debt has increased from £5,545 to £5,711, reaching an all-time high in 2026, according to MoneySuperMarket. It is difficult to be on top of debts every time. It thus leads to missed payments, penalties, and high interest.

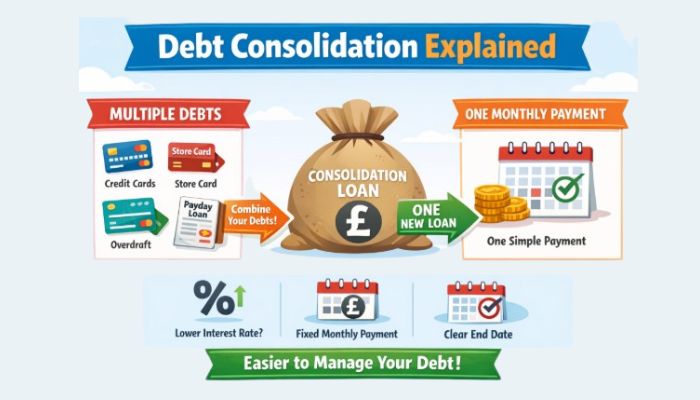

Here, the debt consolidation is a process of merging different debts or payments into a single monthly payment structure. It reduces the interest, monthly payments, and overall cost of the debt.

Instead, it boosts your credit score and helps you achieve your other life goals affordably. However, the loan may not be ideal for everyone. The blog lists the essential aspects about debt consolidation loans to understand.

Key takeaways:

- A debt consolidation involves merging different debts into a single monthly instalment

- Debt consolidation can help save households an average of £1,257 per year in interest.

- Consolidating reduces the monthly instalment and the total amount payable on a debt

- Your monthly debt payments should be lower than 40-50% to get a loan.

- Loan fees may also increase the total repayment costs. Inquire before proceeding.

What is a debt consolidation loan?

A debt consolidation loan helps you merge different debts into one monthly instalment. You can consolidate payday loans, credit card debt, rent, and utility payments all at once in a single arrangement. The purpose of the loan is to reduce the monthly payment liability and improve financial management.

The loan can be secured and unsecured, depending on the needs and the affordability. Individuals with a bad credit score may consider secured loans for debt consolidation to fetch better interest rates. The repayments stay fixed on the loan until the repayment term. You may get £1000-£25000 for a period of 60 months to consolidate the existing debts.

Representative example:

For example, you struggle with paying high-interest credit card and payday loans debt alongside a personal loan. Here are your liabilities and how debt consolidation may help:

- Credit card debt- £5000

- Payday loan debt- £6000

- Personal loan- £15000 (current monthly payment £1200)

- Property value = £350,000

- Mortgage- Nil

Total debt = £26000

New consolidated debt:

If you take a new loan of £26000 for a 10-year repayment term, your monthly repayment will go down from £7,700 to just £282.04. In this way, you pay £7,417.96 less per month!

What should you know about debt consolidation loans?

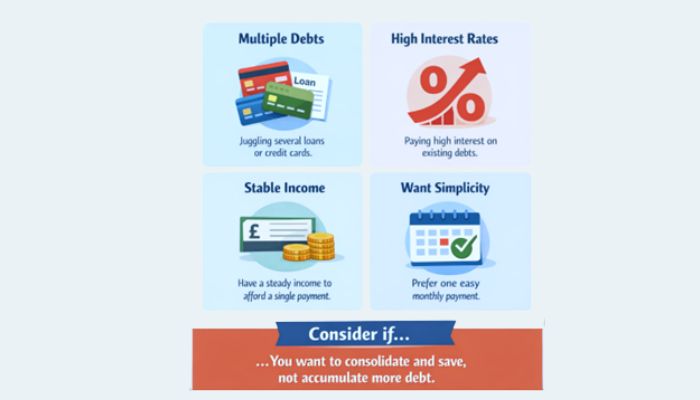

Consolidation may not be ideal for every person. Therefore, it is important to understand the aspects like when to tap, how it works, and the benefits of the loan. Understanding the risks also assists in making the right decision.

Understand the purpose

A Debt consolidation loan has its purpose, just like any other personal loan. It is ideal if you:

- Want to fetch lower interest rates

- Reduce monthly payment liabilities

- Struggle to save for every pending payment separately

- Slash the total amount you must pay on a specific debt

- Want a fixed payment structure to pay the dues by budgeting

It does not guarantee savings

Most individuals believe that debt consolidation is a tool to save money. However, it is not cheaper in every case, particularly with a bad credit score.

For example, if the new loan APR that you get after consolidation is higher than what you currently pay, total interest costs will be higher over time.

At the same time, extending the loan repayment term might provide relief on monthly payments. However, it increases the total interest you must pay on the loan.

It does not require a guarantor

You don’t generally need a guarantor to get a loan for debt consolidation. Individuals with recurring earnings, lengthy employment record, and fair credit scores may qualify. The approval of loans without a guarantor is based on your ability to repay the dues.

You may also get a debt consolidation loan with bad credit without a guarantor if your current finances reveal improvement. However, having a guarantor in this case may help you fetch a higher loan amount and better terms.

How to qualify for a consolidation loan without a guarantor?

- Be regular with your payments by setting direct debits

- Reduce your monthly expenses (cut on unnecessary expenses like dining out, OTT subscriptions)

- Ensure a good credit score by constantly reviewing your finances

- Try to better-up your monthly earnings and

- Bring the debt-to-income ratio to (30:70)

Overspending affects consolidation goals

If you continue to buy things beyond your means, like –

- Applying for a new credit card

- Shopping for luxury items

- Instinctual purchases

- Overspending during festivals, special events like birthdays

It may affect your ability to control debt. Instead, you may get into a debt trap. Therefore, consolidation may not work in this case. You need to ensure responsible financial behaviour by spending only on essentials until you are debt-free.

Impact of debt consolidation on the loan

Consolidating debts can impact your credit score, but if you manage your debts responsibly, the negative impacts will be temporary. Debt consolidation may hurt or help your credit score depending on the method you use and how well you repay the debt.

| How can debt consolidation help your credit score? | How debt consolidation may hurt your credit score? |

| It helps you build a credit history by ensuring on-time payments | Applying for a debt consolidation loan involves a hard credit check, which may affect your credit score temporarily |

| It lowers your credit utilisation ratio by helping you consolidate credit card debt. | Opening new accounts cuts the average accounts age. |

| Helps diversify your credit mix | Consolidating credit cards with balance transfer cards may raise your credit utilisation rate temporarily. |

Risk of losing the property

Not everyone qualifies for an unsecured loan to consolidate debts. Individuals with CCJs, loan defaults, and recent bankruptcy may struggle to get one. It reveals a bad credit state, and hence, one explores the option of debt consolidation with bad credit using an asset. A secured loan may help you qualify instantly for the loan despite a chequered credit history. However, it risks your pricy possession as collateral with the creditor.

You must be confident to repay the dues or your income. Otherwise, missing payments or defaulting on the loan may lead to immediate asset seizure. Thus, identify your potential to repay the dues before confirming the agreement.

High fees may reduce benefits

Some loan providers charge high interest costs, arrangement fees, administrative charges, closure fees, and other hidden fees that may impact the total loan cost. There could be loan fees from the original credit providers on debts that you want to consolidate. Thus, it may make the loan costly for most people and hence affect the benefits.

It is thus always important to check the total loan costs rather than just relying on interest and APR. You can prequalify with the best loan providers to understand the total cost of a loan and decide accordingly. Always inquire about hidden costs (if any) from the creditor, or anything that you don’t understand. It may help you save enough money in the long run.

Bottom line

Thus, getting a loan for debt consolidation in the UK requires you to analyse the basics first. Understand the purpose, loan eligibility criteria, and how the whole process works. It will help you understand the debts that you may benefit from consolidating. The aim of consolidation is to remain on top of your debt payments.

Sarah Jones is a seasoned financial writer with over a decade of experience covering personal finance loans, and dedicated to provide the best lending solutions to the clients. Known for translating complex financial topics into accessible insights, Sarah contributes to leading loan providers like Arbitrageloans and contributes to the company’s growth via professional writing and loan guidance. She holds a degree in economics and is passionate about helping aspirants with tools to make informed loan decisions. She also loves to explore the world and its natural beauty. Sarah believes financial literacy is the base of legitimate lending and borrowing. She strives to make it understandable for all.